HOME

9/22/2005 - 1/23/2016 - 100+ supporting documents found at menu item "Document List". These include Doc 12, Doc 13 and Doc 14 which are 30 pages of transcribed emails with BofA Execs and BofA Legal which detail the nefarious games in writing.( Doc12a, Doc13a, Doc14a, and Doc14b are the original emails )

====================================================================================================

====================================================================================================

====================================================================================================

====================================================================================================

1/24/2016 - Bank of America Responded to a Consumer Financial Protection Bureau (CFPB) complaint filed in December 2015 related to 3 items below - Click Here for BofA Response to Complaint

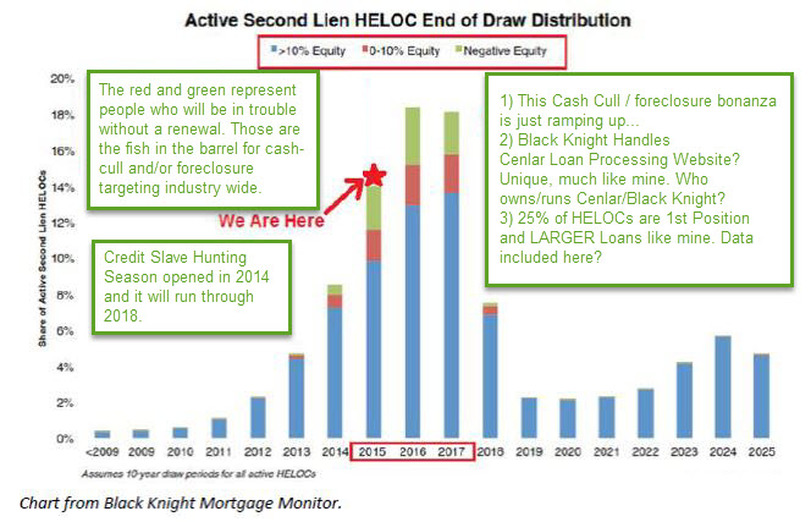

- Bank of America arbitrarily refused to execute HELOC Renewals. The "seemingly" arbitrary denial of a renewal is in fact anything but arbitrary. In truth, it is the initiation of a Credit Slave Hunt in disguise. This hunt targets 3.3 Million high credit homeowners. It is estimated to net 66,000 foreclosures and $15 Billion per year in cash constriction. details | details with a Slave Trade Theme and Graph

- After the arbitrary denial of a Renewal, which created a scenario in which my $900/month payment was going to adjust to $2600/month, Bank of America offered a Modification Application Process to reduce payment adjustment shock. (arbitrarily shove me in only to partially bail me out? suspicious...) The Modification Application Process turned out to be a fake, for outward appearances only. BofA Execs had created a very well choreographed Fraudulent Underwriting Denial Process to deny those they invited to apply. Over 20 Regulation Z Truth in Lending Act violations related to a fraudulent Ability-to-Repay analysis were documented in 30 pages of emails with Bank of America Executives details

- Per items 1 and 2 above, Bank of America is engaged in Racketeering Activities Internally and Industry Wide -- 8 levels of bankers in four geographic locations were touched by my communication on this matter ( 1 customer service agent, 2 VPs, 2 SrVPs, 1 Assistant General Counsel, 1 Enterprise Customer Service Agent, 1 Enterprise Customer Service Manager, 1 Brian Moynihan (CEO), and 1 Anne Funicane (Vice Chairman) ) -- (North Carolina, New Hampshire, California, and Boston). Each of these individuals was involved at some level in activities related to Conspiracy to Commit Fraud, Fraud, Wire Fraud, Mail Fraud, Making False Statement to Customers, Conspiracy to Cover Up Fraud, Conversion and others details

OVERSIGHT FAILURE--ELIZABETH WARREN- RICHARD SHELBY--SHERROD BROWN--MANY MORE..

OVERSIGHT FAILURE--ELIZABETH WARREN- RICHARD SHELBY--SHERROD BROWN--MANY MORE..

In September 2015 my first notices related to this matter went to Senator Richard Shelby, Senator Sherrod Brown, Vice President Joe Biden and President Barack Obama. Within a few days, the CEO of Bank of America, 200 bankers, and national and international media were notified if my concerns related to this via email ( http://bofa-bunker-buster.weebly.com/ ) and within a few more days every US Senator, Congressman and State Governor was notified by me digitally about this situation via one method or another.

In October 2015 this website was launched to enable those in Government to keep the focus of this on Bank of America and our for profit banks, with less focus on the FED involvement, in hopes the could/would do something about this situation.

In December 2015 my information made it to the Consumer Financial Protection Bureau (the CFPB) in the form of a formal complaint. Around that time, I thought for sure Elizabeth Warren would swoop in for the KILL. She didn't. It was odd and telling. Subsequently, her failure to endorse Bernie came as no surprise to me as I got a peek behind the curtain before the other commoners did.

The CFPB and Senator Elizabeth Warren -- The CFPB was spearheaded by Senator Elizabeth Warren. Her inaction on this matter given the information I sent to her directly, submitted to the CFPB and that which I've published online since the fall of 2015 is beyond startling. Elizabeth is well respected by many as an Attorney with deep banking background and care for the middle class. She has shown her ability to "figure out" complex banking scams (see video below). She was given everything needed to know exactly what I was screaming about, and yet she took no action. Nor did anyone else.

Why haven't you stepped in Elizabeth? The "solution" to this HELOC Reset crisis can be summed up in 1 sentence. No Gov't oversight required, not Gov't funds required. The solution is "Issue HELOC renewals as has been the case for all times prior to now"... BUT if the solution was pursued, it would reverse the goal of the National Cash Constriction that it was intended to create... hummm... what a conundrum....

So who's going to spill the beans on what's what in Washington? Elizabeth? Richard? Sherrod? Joe? Barack? Who's going to do the honors? Paul Ryan is touted as a math guru... Will he let cat out of bag?

Elizabeth's failure to endorse Bernie in the 2016 Presidential Campaign was perplexing to many given a seemingly shared passion for Banker problems. And then it happened. Her endorsement of HRC was down-right GOBSMACKING. That was like de ja vu in the Matrix.

In 2004 Elizabeth called out HRC for caving to the Lobbying Pressures of Consumer Bankers once she became a Senator (video below) . According to Warren in 2004, Consumer Bankers related to Credit markets were by far the largest lobbying group in the Country. But is it really just about Bankers dumping money into campaign finance for profits or is there something more about "control of the country" that gets fed into the indoctrination routine?

Elizabeth, would you like to elaborate on what you found out about banking between 2004 and 2016 that turned that idealistic woman below into an HRC supporter with the cloak of a bad-ass Banking Cop?

Elizabeth, would you like to tell us a little now about the true Agenda and the true reach of those who are members of The Counsel on Foreign Relations now?

Matt Damon may need to revise his pick for bad-ass banking cop after this...

======================================================================================================

======================================================================================================

1/31/2016 - In response to Bank of America's response to these matters on 1/24/2016, the docs below were uploaded to the CFPB console ( Pic of console ). These documents lay out the entire Fraud A to Z. These documents do NOT detail anything related to Regulation Z of the Truth in Lending Act nor the Bulletin from the OCC which connects the OCC and the FED to the HELOC Reset Crisis. I did not connect that information to my own publishing until June 2016. Given Senator Elizabeth Warren is an Attorney focused on banking fraud, she should have been able to make the proper connections to Regulation Z of the Truth in Lending Act and the July 2014 OCC Bulletin without my hand holding. Her inaction on this matter thus far has been telling.

2/4/2016 - Fax to Congressman Sarbanes et al notifying them that my information had made it into the Federal System (via CFPB Case) under penalty of perjury - Click Here

2/15/2016 - Notice to BofA of Fair Credit Reporting Act Violations and consumer driven payment modification supported by Page 10 of our Agreement - Click Here

2/15/2016 - Notice to Congressmen and Senators of the Fair Credit Reporting Act as it relates to a Consumer Driven Payment Modification reality and the Potential for HUGE fines - Click Here

2/16/2016 - Bar Grievance Filing with Alabama, South Carolina and North Carolina State Bars as it pertains to Bank of America Assistant General Counsel David K. Tinkler - Click Here

3/7/2016 - Bar Grievance Re-submission to Alabama, South Carolina, and North Carolina Bar identifying specific Rule of Conduct Violations of Bank of America Assistant General Counsel David K. Tinkler - Click Here

4/20/2016 - Bar Grievance Filing Response from the Alabama Bar with the response forced from Bank of America Assistant General Counsel David K. Tinkler -- Click Here

6/14/2016 - Bar Grievance Filing - TAKE 3 - Alabama Bar -- Click Here

6/14/2016 - Bar Grievance Filing - TAKE 3 - South Carolina Bar -- Click Here

6/14/2016 - Fax to some GREAT folks - Cumulative update related to past 4 months of activities. 1) Notice of Public Disclosure of the July 2014 OCC Bulletin which in fact was the command to start the HELOC-Reset-Crisis (contrary to its outward appearance) and notice of HELOC Reset Crisis Unmasked website 2) notice regarding Regulation Z of the Truth In Lending Act with regards to all aspects of Open and Closed Credit and BofA fraud, 3) BAR dialogue/Grievance Update 4) My experience at 3 presidential candidate rallies 5) formal notice of my-day-at-HRC-rally website 6) notice of naked bankers on parade website 7) Elizabeth Warren (omg, wth?) 8) update for this website's content 9) Weebly and Gdrive updates 10) Fear, the vanishing power 11) MSM hit piece on HRC and Security Counsel Appointee (from 2011?) 12) Pyramids and neural networks 13) AI 14) AWAKE, Repub or Dem meme 15) LOVE Trains 16) Bernie as Winner of Hearts and Minds 17) Great new media publishing co 19) Jill Stein is cool 18) Beau's final act 19) Click... Click... Click... 20) Andrew Jackson was a bad-ass 21) Sounds in the silence 22) Shortened transition period 23) This is all their fault!! and some other stuff. -- Click here (link will go live sometime in the future)

- Dispute Doc 0 of 6 - Abstract - 8 pages - Click Here

- Dispute Doc 1 of 6 - The Big Picture w/ References to 80 supporting docs - 25 pages - Click Here

- Dispute Doc 2 of 6 - Dissection of BofAs CFPB response dtd 1/21/2016 - 16 pages - Click Here

- Dispute Doc 3 of 6 - This Situation in "Legalese" - 7 pages - Click Here

- Dispute Doc 4 of 6 - Discovery Questions - 15 pages - Click Here

- Dispute Doc 5 of 6 - Fil Sarabia - Your CFPB response was very inappropriate - 3 pages - Click Here

- Dispute Doc 6 of 6 - Art of War - 1 page - Click Here

The documents above and the text below have red references like "Doc 5". Those supporting documents are part of the 80+ supporting docs found at menu item "Document List".

2/4/2016 - Fax to Congressman Sarbanes et al notifying them that my information had made it into the Federal System (via CFPB Case) under penalty of perjury - Click Here

2/15/2016 - Notice to BofA of Fair Credit Reporting Act Violations and consumer driven payment modification supported by Page 10 of our Agreement - Click Here

2/15/2016 - Notice to Congressmen and Senators of the Fair Credit Reporting Act as it relates to a Consumer Driven Payment Modification reality and the Potential for HUGE fines - Click Here

2/16/2016 - Bar Grievance Filing with Alabama, South Carolina and North Carolina State Bars as it pertains to Bank of America Assistant General Counsel David K. Tinkler - Click Here

3/7/2016 - Bar Grievance Re-submission to Alabama, South Carolina, and North Carolina Bar identifying specific Rule of Conduct Violations of Bank of America Assistant General Counsel David K. Tinkler - Click Here

4/20/2016 - Bar Grievance Filing Response from the Alabama Bar with the response forced from Bank of America Assistant General Counsel David K. Tinkler -- Click Here

6/14/2016 - Bar Grievance Filing - TAKE 3 - Alabama Bar -- Click Here

6/14/2016 - Bar Grievance Filing - TAKE 3 - South Carolina Bar -- Click Here

6/14/2016 - Fax to some GREAT folks - Cumulative update related to past 4 months of activities. 1) Notice of Public Disclosure of the July 2014 OCC Bulletin which in fact was the command to start the HELOC-Reset-Crisis (contrary to its outward appearance) and notice of HELOC Reset Crisis Unmasked website 2) notice regarding Regulation Z of the Truth In Lending Act with regards to all aspects of Open and Closed Credit and BofA fraud, 3) BAR dialogue/Grievance Update 4) My experience at 3 presidential candidate rallies 5) formal notice of my-day-at-HRC-rally website 6) notice of naked bankers on parade website 7) Elizabeth Warren (omg, wth?) 8) update for this website's content 9) Weebly and Gdrive updates 10) Fear, the vanishing power 11) MSM hit piece on HRC and Security Counsel Appointee (from 2011?) 12) Pyramids and neural networks 13) AI 14) AWAKE, Repub or Dem meme 15) LOVE Trains 16) Bernie as Winner of Hearts and Minds 17) Great new media publishing co 19) Jill Stein is cool 18) Beau's final act 19) Click... Click... Click... 20) Andrew Jackson was a bad-ass 21) Sounds in the silence 22) Shortened transition period 23) This is all their fault!! and some other stuff. -- Click here (link will go live sometime in the future)

Brief Intro to CFPB Case related to Bank of America Racketeering and Industry Wide Collusion

On 12/21/2015 CFPB Case 151221000345 was opened regarding my claims regarding Racketeering at BofA and Industry Wide Collusion related to the fully bank contrived HELOC Reset Crisis that is quietly playing out from 2014-2018, that will affect 3.3 million consumers. Approximately $15 billion/year is being frocibly removed from the pockets of "A paper" middle income citizens for bank profits and demonstration of consumer credit control to create stress and fear in our society. We can expect approximately 66,000 foreclosures from this artificial cash cull, and the decrease in consumer spending across the country will be cumulative for the next 3 years ($15/$30/$45 billion in reduced consumer spending).

My personal experience is related to an arbitrary freeze of a my credit line due to the lack of a Renewal Application process which was promised at time of origination, and part of the banks standard operating procedures at time of origination. This arbitrary denial of a Renewal results in the conversion of my $315,000 account balance to an installment loan with a 15 year, non-amortizing repayment term, which results in a $1750/month forced account paydown (plus standard monthly interest). My $841 payment just jumped to $2600/month. The math alone tells you something is dramatically wrong here. When you understand all the facts related to the nefarious work to arbitrarily deny renewals, you will see this forced paydown is the result of a clever form of Extortion/Conversion (civil law's definition of theft/borrowing for their own good).

Furthermore, when you realize ALL BIG BANKS are behaving in a similar, non-natural manner related to the denial of renewal applications, you will realize we are actually dealing with a case of industry wide collusion. And it gets nastier.

After being forced into the installment loan conversion pipeline, BofA offered a repayment term extension application process via a form letter which would have extended the 15 year repayment term to 25 (and that would have reduced my pending $2600/mo payment to $1900/mo). Unfortunately, this public offer of potential relief was for outward appearances only. A BofA employee executed a false denial for the underwriting process via a fully choreographed false denial script and a fabricated debt value. Upon escalation to a VP, she attempted to deliver a second false denial process by introducing a nonsensical dual debt-income ratio requirement which was not transparent in the first denial and would be deemed totally nefarious by anyone with underwriting background. (Doc 12, Doc 13).

Four levels of VPs were given the opportunity to address this situation and they all refused (Doc 12, Doc 13). When David Tikler, BofA Legal, was confronted in writing (Doc 14), I was presented with an offer for the Repayment Term Extension I had been falsely denied, with a non-disclosure agreement attached. That was a BRIBE for silence. The gist goes something like this, "We'll give you the payment reduction we fraudulently denied, as long as you don't tell anybody about what we are doing".

My personal experience is related to an arbitrary freeze of a my credit line due to the lack of a Renewal Application process which was promised at time of origination, and part of the banks standard operating procedures at time of origination. This arbitrary denial of a Renewal results in the conversion of my $315,000 account balance to an installment loan with a 15 year, non-amortizing repayment term, which results in a $1750/month forced account paydown (plus standard monthly interest). My $841 payment just jumped to $2600/month. The math alone tells you something is dramatically wrong here. When you understand all the facts related to the nefarious work to arbitrarily deny renewals, you will see this forced paydown is the result of a clever form of Extortion/Conversion (civil law's definition of theft/borrowing for their own good).

Furthermore, when you realize ALL BIG BANKS are behaving in a similar, non-natural manner related to the denial of renewal applications, you will realize we are actually dealing with a case of industry wide collusion. And it gets nastier.

After being forced into the installment loan conversion pipeline, BofA offered a repayment term extension application process via a form letter which would have extended the 15 year repayment term to 25 (and that would have reduced my pending $2600/mo payment to $1900/mo). Unfortunately, this public offer of potential relief was for outward appearances only. A BofA employee executed a false denial for the underwriting process via a fully choreographed false denial script and a fabricated debt value. Upon escalation to a VP, she attempted to deliver a second false denial process by introducing a nonsensical dual debt-income ratio requirement which was not transparent in the first denial and would be deemed totally nefarious by anyone with underwriting background. (Doc 12, Doc 13).

Four levels of VPs were given the opportunity to address this situation and they all refused (Doc 12, Doc 13). When David Tikler, BofA Legal, was confronted in writing (Doc 14), I was presented with an offer for the Repayment Term Extension I had been falsely denied, with a non-disclosure agreement attached. That was a BRIBE for silence. The gist goes something like this, "We'll give you the payment reduction we fraudulently denied, as long as you don't tell anybody about what we are doing".

The BofA Execs directly involved in this nefarious work are:

- David Tinkler, Assistant General Counsel, Legal Department-Bank of America

- Karen Spagna, SVP - Home Equity Underwriting and Fulfillment Executive

- Jennifer Bone, SVP - Performance Executive

- Dwight Carlisle, VP - Fulfillment Unit Leader

- Betty Watson, VP - Team Manager

- Email addresses and phone numbers for them can be found at "BofA Details/Contact Info for BofA Execs"

- Very detailed email dialogue with all of these individuals included on the BofA Details menu

- Fil Sarabia, Enterprise Customer Service (Added 1/23/2016 and full name possibly Marie Fil Sarabia)

- Daniel Whitehead, Enterprise Customer Service Manager (Added 6/14/2016 after mucking up the modification without a non-disclosure and committing two more acts of fraud in the process http://naked-bankers-on-parade-2016.weebly.com/ )

As mentioned at the beginning, this isn't a 1 off situation. I'm one of 750,000 people BofA may be doing this too in the next 3 years, and I'm one of 3.3 million facing HELOC resets across the industry in the next 3 years and ALL are getting rolled from Lines of Credit (open end credit) into these installment loan conversion situations (closed end credit) in a non-natural manner. I have provided documents and factual proof of this same type of thing transpiring at PNC Bank as well as Harris Bank, and when you compare Bank of America Docs to PNC docs, the Industry Collusion becomes overtly apparent.

Time Line - 2005 to present

There are 80+ supporting docs for all the info below...

2005 - HELOC originated for $315,000 in 1st lien position at about 75% of property value. At time of origination, it was noted that all Big Banks were convoluting HELOC Agreements by dumbing down and/or removing renewal clauses and tweaking then irrelevant repayment terms in non-natural ways. BofA had added prominent repayment term text above the renewal clause which was "superfluous" in their day to day activities then and likewise was "superfluous" given their promises of a risk based Renewal Application Process at time of Reset review in 2015.

2008 - HELOC arbitrarily frozen and released 2 weeks later after passionate letter written

August 2014 - First notice of Reset from BofA for $315,000 HELOC in 1st position on my property - no renewal option - implication is repayment term is only option - $841 payment would adjust to $2615 on 9/27/2015

November 2014 - First notice of Reset from PNC Bank for two HELOCs in 2nd position on two properties - no renewal option - implication is a repayment term is only option - payments TRIPLING - similar to Bofa - BUT they offered a one page modification process at end of notice that required check mark and signature to avoid the TRIPLING situation. While I wanted a renewal, this was a gift of epic proportions, so I took what I could get, realizing now all the banks were into some very nefarious games.

November 2014 through February 2015 - Called BofA on several occasions requesting an opportunity to apply for a Renewal. An opportunity that had been promised at time of origination. Denied every time.

April 2015 - Second notice of Reset from Bofa. No Renewal Application option, BUT this included a Repayment Term Extension that would reduce that pending $2615 payment to $1900.

May-June 2015 - 1 month in underwriting culminated in a fake denial process. An inflated debt value was used to create a fake Debt-Income ratio. When questioned why the debt value was ~$300 higher than it should have been, Agent didn't have any info related to the calculated debt value, and she tried to redirect conversation to income, which she had every detail for. The script used for this fake denial process was fully choreographed. Upon escalation to a VP, she attempted to use a different fake denial process by revealing that the ratio presented was NOT related to the 25 year repayment term I was applying for, but that is was the relevant ratio in the denial process. The ratio used for the denial was not related to my current debt nor my proposed debt. The ratio used for the denial was related to a 15 year repayment term which was the term I was trying to avoid (and not my current debt nor my proposed debt). Not much different than picking a number out of the blue, but this one will confuse many who aren't familiar with standard underwriting procedures. UTTER INSANITY. After going thru this, I found documentation of similar false denial processes as confessed to by BofA Whistle Blowers (Doc 20, Doc 20a). Emails with 4 levels of BofA Execs (Doc 12, Doc 13)

July 2015 - Emails with David Tinkler, BofA Asst. General Counsel (Doc 14) . David sends a very careless email in which he attempts to explain away the lack of a renewal process as an arbitrary "matter of policy" change. David used non-risk based logic to explain away a side conversation about income adjustments. The income adjustment conversation becomes relevant to prove BofA had no intentions of approving anyone for their Repayment Term Extension application. Basically, if the first two denials failed, they would create other false excuses ad hoc to attempt to keep customers in the trap. David was called out on all nefarious fronts in writing, and the following day David extended an offer for the repayment term I was fraudulently denied contingent I sign a non-disclosure agreement. Given there is NEVER a time when transparent underwriting should require a non-disclosure agreement, you can be confident this offer is in fact a case of attempted Black Mail. The general gist was, " We'll give you the payment reduction we fraudulently denied on the installment loan we've arbitrarily forced you into as long as you don't tell anyone about what we are doing". I denied that offer, which would have reduced my pending $2600 monthly payment to $1900/month to be the voice for 3.3 million citizens.

October 20, 2015 - This website launched after other attempts to get BofA to clean up their own house failed.

November 6, 2015 - Congressman Sarbanes forwarded info to the CFPB regarding my situation.

December 21, 2015 - The Initial Complaint was entered by the CFPB on my behalf. ( Doc 47 ) The text for the complaint was entered from an email I sent to Congressman Sarbanes that was solely intended to get his attention, with Big Picture facts. That text did not have the type of written details and/or request for information in it that I would have liked to have seen for an initial submission to BofA on my behalf from the CFPB, but oh well. We are on our way now...

January 21, 2016 - Fil Sarabia of Bank of America uploaded a very careless, misleading and self-incriminating response to the CFPB console ( Doc 73a ). From her response no reader would realize she and I had a 45 minute conversation about the nitty-gritty details related to the fake denial processes, the fake debt values, the complex but poorly configured customer service scripts that a confirmed the scam, the second fake denial attempt by a VP with an alternate strategy, the lie made by the VP that was recanted, nor the Industry Wide Collusion with BofA and PNC Bank as an example. From her response, no reader would also realize she confirmed receipt of a URL with 40+ documents (a link to the webpage at "CFPB Case ...0345") which included Statement of Facts #1, #2, #3 and 40+ factual documents supporting those statement of facts (Doc 46 is the fax sent to her, and Doc 48 his her confirmation of that fax). I've directly addressed Fils insincerity in Dispute Doc 5 of 6 - Please see Doc 73a for Fil's fucking pathetic 3 page response to this very serious personal and now federal matter. With her response, Fil is now a part of the conspiracy to cover up fraud. Fil closed her response with "We have reviewed your claims and our research has uncovered no specific facts which would substantiate a claim of racketeering. If you would like me to investigate your concerns further, we will need you to provide specific, factual information in support of your claims ". What foolishness. I have a solution for that. Ask, and yeah shall receive...

January 31, 2016 - I uploaded Dispute Doc 0 of 6 through Dispute Doc 6 of 6 (available above) to the CFPB as my dispute to BofAs response to the CFPB on this matter. Since receiving BofA's response on 1/21/2016 I increased the reference docs on this website from 40+ to 80+, AND I wrote 70+ pages (Dispute Docs at top of page) with full references to the 80+ supporting documents to provide a "trail map" and "absolute clarity" on this matter for BofA and all others who will get involved. I decided removing feigned ignorance, feigned incompetence and almost every other excuse and defense position imaginable from the table was going to be the best approach to spotlighting this very nefarious situation. In Dispute Doc 3 and Dispute Doc 4 I've tried to provide the framework needed for both a civil/criminal claim (all be it unprofessional as I have no formal legal training) as well as deposition questions to further frame the nature of the deviance and to expedite Federal intervention on this matter. It's time to pick up a sincere dialogue, and fast. I'm over the games. In Doc 1 of 6 I've put a February 12, 2016 deadline in for short term relief from BofA for my personal situation, and I've shared an energetic leverage strategy I will employ if I don't get the short term relief I'm seeking personally. If BofA does not get sincere quickly, this isn't a matter for the courts. This is justification to pull their Federal Banking Charter. Possessing a Federal Banking Charter is a privilege, it is not a right, and everything needed to do that is contained in my supporting documents. 33 pages of two way email dialogue transpired with BofA while this played out. If this was related to a "miscommunication" or a disagreement on "simple math", that was their time to present their position. Furthermore, if this was about a "miscommunication" or "simple math", they had every opportunity to clarify those details in their CFPB response instead of providing 30-60 pages of computer screen shots which say nothing and which they didn't make one reference to in their response. Bank of America did a bang up job of incriminating themselves in Doc 12, Doc 13 and Doc 14, and it actually continued with their CFPB response Doc73a. Those documents alone should convince everyone something is wrong. My documents simply explain the what, why and how of it.

February 4, 2016 - Congressman Sarbanes, Senator Sanders, Senator Warren, Senator Paul and others were notified that the info that was previously limited to all my website content had been consolidated in the form of Dispute Docs and they had been officially entered into the Federal System, under penalty of perjury, on January 31, 2016.

2005 - HELOC originated for $315,000 in 1st lien position at about 75% of property value. At time of origination, it was noted that all Big Banks were convoluting HELOC Agreements by dumbing down and/or removing renewal clauses and tweaking then irrelevant repayment terms in non-natural ways. BofA had added prominent repayment term text above the renewal clause which was "superfluous" in their day to day activities then and likewise was "superfluous" given their promises of a risk based Renewal Application Process at time of Reset review in 2015.

2008 - HELOC arbitrarily frozen and released 2 weeks later after passionate letter written

August 2014 - First notice of Reset from BofA for $315,000 HELOC in 1st position on my property - no renewal option - implication is repayment term is only option - $841 payment would adjust to $2615 on 9/27/2015

November 2014 - First notice of Reset from PNC Bank for two HELOCs in 2nd position on two properties - no renewal option - implication is a repayment term is only option - payments TRIPLING - similar to Bofa - BUT they offered a one page modification process at end of notice that required check mark and signature to avoid the TRIPLING situation. While I wanted a renewal, this was a gift of epic proportions, so I took what I could get, realizing now all the banks were into some very nefarious games.

November 2014 through February 2015 - Called BofA on several occasions requesting an opportunity to apply for a Renewal. An opportunity that had been promised at time of origination. Denied every time.

April 2015 - Second notice of Reset from Bofa. No Renewal Application option, BUT this included a Repayment Term Extension that would reduce that pending $2615 payment to $1900.

May-June 2015 - 1 month in underwriting culminated in a fake denial process. An inflated debt value was used to create a fake Debt-Income ratio. When questioned why the debt value was ~$300 higher than it should have been, Agent didn't have any info related to the calculated debt value, and she tried to redirect conversation to income, which she had every detail for. The script used for this fake denial process was fully choreographed. Upon escalation to a VP, she attempted to use a different fake denial process by revealing that the ratio presented was NOT related to the 25 year repayment term I was applying for, but that is was the relevant ratio in the denial process. The ratio used for the denial was not related to my current debt nor my proposed debt. The ratio used for the denial was related to a 15 year repayment term which was the term I was trying to avoid (and not my current debt nor my proposed debt). Not much different than picking a number out of the blue, but this one will confuse many who aren't familiar with standard underwriting procedures. UTTER INSANITY. After going thru this, I found documentation of similar false denial processes as confessed to by BofA Whistle Blowers (Doc 20, Doc 20a). Emails with 4 levels of BofA Execs (Doc 12, Doc 13)

July 2015 - Emails with David Tinkler, BofA Asst. General Counsel (Doc 14) . David sends a very careless email in which he attempts to explain away the lack of a renewal process as an arbitrary "matter of policy" change. David used non-risk based logic to explain away a side conversation about income adjustments. The income adjustment conversation becomes relevant to prove BofA had no intentions of approving anyone for their Repayment Term Extension application. Basically, if the first two denials failed, they would create other false excuses ad hoc to attempt to keep customers in the trap. David was called out on all nefarious fronts in writing, and the following day David extended an offer for the repayment term I was fraudulently denied contingent I sign a non-disclosure agreement. Given there is NEVER a time when transparent underwriting should require a non-disclosure agreement, you can be confident this offer is in fact a case of attempted Black Mail. The general gist was, " We'll give you the payment reduction we fraudulently denied on the installment loan we've arbitrarily forced you into as long as you don't tell anyone about what we are doing". I denied that offer, which would have reduced my pending $2600 monthly payment to $1900/month to be the voice for 3.3 million citizens.

October 20, 2015 - This website launched after other attempts to get BofA to clean up their own house failed.

November 6, 2015 - Congressman Sarbanes forwarded info to the CFPB regarding my situation.

December 21, 2015 - The Initial Complaint was entered by the CFPB on my behalf. ( Doc 47 ) The text for the complaint was entered from an email I sent to Congressman Sarbanes that was solely intended to get his attention, with Big Picture facts. That text did not have the type of written details and/or request for information in it that I would have liked to have seen for an initial submission to BofA on my behalf from the CFPB, but oh well. We are on our way now...

January 21, 2016 - Fil Sarabia of Bank of America uploaded a very careless, misleading and self-incriminating response to the CFPB console ( Doc 73a ). From her response no reader would realize she and I had a 45 minute conversation about the nitty-gritty details related to the fake denial processes, the fake debt values, the complex but poorly configured customer service scripts that a confirmed the scam, the second fake denial attempt by a VP with an alternate strategy, the lie made by the VP that was recanted, nor the Industry Wide Collusion with BofA and PNC Bank as an example. From her response, no reader would also realize she confirmed receipt of a URL with 40+ documents (a link to the webpage at "CFPB Case ...0345") which included Statement of Facts #1, #2, #3 and 40+ factual documents supporting those statement of facts (Doc 46 is the fax sent to her, and Doc 48 his her confirmation of that fax). I've directly addressed Fils insincerity in Dispute Doc 5 of 6 - Please see Doc 73a for Fil's fucking pathetic 3 page response to this very serious personal and now federal matter. With her response, Fil is now a part of the conspiracy to cover up fraud. Fil closed her response with "We have reviewed your claims and our research has uncovered no specific facts which would substantiate a claim of racketeering. If you would like me to investigate your concerns further, we will need you to provide specific, factual information in support of your claims ". What foolishness. I have a solution for that. Ask, and yeah shall receive...

January 31, 2016 - I uploaded Dispute Doc 0 of 6 through Dispute Doc 6 of 6 (available above) to the CFPB as my dispute to BofAs response to the CFPB on this matter. Since receiving BofA's response on 1/21/2016 I increased the reference docs on this website from 40+ to 80+, AND I wrote 70+ pages (Dispute Docs at top of page) with full references to the 80+ supporting documents to provide a "trail map" and "absolute clarity" on this matter for BofA and all others who will get involved. I decided removing feigned ignorance, feigned incompetence and almost every other excuse and defense position imaginable from the table was going to be the best approach to spotlighting this very nefarious situation. In Dispute Doc 3 and Dispute Doc 4 I've tried to provide the framework needed for both a civil/criminal claim (all be it unprofessional as I have no formal legal training) as well as deposition questions to further frame the nature of the deviance and to expedite Federal intervention on this matter. It's time to pick up a sincere dialogue, and fast. I'm over the games. In Doc 1 of 6 I've put a February 12, 2016 deadline in for short term relief from BofA for my personal situation, and I've shared an energetic leverage strategy I will employ if I don't get the short term relief I'm seeking personally. If BofA does not get sincere quickly, this isn't a matter for the courts. This is justification to pull their Federal Banking Charter. Possessing a Federal Banking Charter is a privilege, it is not a right, and everything needed to do that is contained in my supporting documents. 33 pages of two way email dialogue transpired with BofA while this played out. If this was related to a "miscommunication" or a disagreement on "simple math", that was their time to present their position. Furthermore, if this was about a "miscommunication" or "simple math", they had every opportunity to clarify those details in their CFPB response instead of providing 30-60 pages of computer screen shots which say nothing and which they didn't make one reference to in their response. Bank of America did a bang up job of incriminating themselves in Doc 12, Doc 13 and Doc 14, and it actually continued with their CFPB response Doc73a. Those documents alone should convince everyone something is wrong. My documents simply explain the what, why and how of it.

February 4, 2016 - Congressman Sarbanes, Senator Sanders, Senator Warren, Senator Paul and others were notified that the info that was previously limited to all my website content had been consolidated in the form of Dispute Docs and they had been officially entered into the Federal System, under penalty of perjury, on January 31, 2016.

The Racketeering - BofA Style

Bank of America Employees are arbitrarily denying HELOC renewals to force customers into installment loan conversions with a predatory repayment period. They are then going to extreme lengths to keep people in these predatory repayment periods, while presenting the outward appearance of working with customers. The Docs I have uploaded support crimes related to False Advertising, Conspiracy to Commit Fraud, Fraud, Mail Fraud, Extortion and attempted Black Mail. I do NOT look likely on making these types of claims on a website especially when I then follow them up with the names of BofA Execs and employees who are involved in these crimes: David Tinkler (Assistant General Counsel), Karen Spagna (SVP), Jen Bone (SVP), Dwight Carlise (VP), Betty Watson (VP), and Latece Campbell (Customer Service Agent). Given the dialogue and docs that were provided to Fil Sarabia (Enterprise Customer Service) and given her response to a Federal Agency which implies we never had dialogue and that she was not provided with access to factual docs to support my racketeering claims (like 33 pages of emails with BofA execs), she, in my opinion, is now also Conspiring to Cover Up Fraud. Companies don't commit crimes. People do, and it's time to start prosecuting the people committing the crimes. Daniel Whitehead (Enterprise Customer Service Manager) earned his spot in the record books due to nefariously handling the modification without the non-disclosure, once that time finally arrived.

Other Commentary

You are at the entrance of a very deep rabbit hole. The good news is I've provided trail maps in the form of Dispute Docs that make it relatively easy to explore this very nefarious, industry wide banking phenomena with 80+ reference documents. The even better news is that this is a scam that was setup a decade ago and that has been going on for the past 2 years, is currently in process, and would/could have gone on for another 2 years had this outing not been initiated. And that is all good news because when things are happening in real time vs in the past, its a lot harder for the nefarious bunch to wiggle out.

The documents above were uploaded to the CFPB console on 1/31/2016. Notifications were sent to several relevant parties of these documents on 1/31/2016. I'm hoping/expecting to get some short term personal relief on this from Bank of America by February 12, 2016. (Detailed in Dispute Doc 1 of 6). After that, I'll be working to assist others with relief if our Government and/or our society doesn't pick up the ball first (which is my hope). Senator Shelby, Senator Sherrod Brown, Senator McCain and the White House has known about this since September, so it shouldn't be new news to them. Hopefully now that this has officially been submitted to a Federal Government Agency, that will provide the confidence they need to move forward with regards to this situation.

Start with Dispute Doc 0 of 6. Then move on to Dispute Doc 1 of 6. After that, the rest is a lot of details you can skim or read as you see fit.

For the full unveiling with the July 2014 OCC Bulletin Information and Regulation Z of the Truth in Lending Act included, see http://the-heloc-reset-crisis-unmasked.weebly.com/

For Homeowners and those in Economic Development

This affects every community in the country. My disposable income dropped by $1750/month and I"m just one of 3.3 Million people caught in this trap. That's a lot less stimulus in my local economy. I am an extreme case. HELOCs by nature are a checking account, credit card, debit card, interest bearing savings account and an interest only mortgage substitute, all in a single banking product. If you don't know how HELOCs work, you have no clue what you've been missing. In this case, what's good for the consumer is very bad for the "for-profit" bankers profit model. Once you understand that, you will then understand exactly why Bankers are doing everything in their power to muck-up originating, servicing and renewing HELOC Accounts for arbitrary reasons. The ultimate goal is to destroy the product in pure form and it's reputation to sustain our current, non-natural closed end Mortgage Industry, which is a Debt Slave Trade in disguise. The best way to get a consumer not to use a product that is best for them is to get them to fear it themselves. The goal with this complaint short term is to stop the nefarious resets and reverse the damage done to citizens over the past 2 years. The long term goal is to find a better solution for HELOC origination and servicing, outside of the current "for-profit" banker paradigm. Such a move would tank the Mortgage Industry and Greedy for Profit Bankers. They had their opportunity to be "reasonable" by watering the grass on their own playing field. They failed to water the grass. Instead, they chose to sell their water for profits, and they chose to pollute it for profits. No longer any need to keep the parched playing field around.